Should You Combine Finances with Your Partner? Pros, Cons, and Modern Alternatives

In today’s evolving landscape of relationships and financial management, whether or not to combine finances with a partner remains a subject of important discussion. With nearly 50% of marriages in the US ending in divorce, financial disputes are often cited as one of the leading causes of relationship strain. Merging financial lives seems like a natural step for many couples, symbolizing trust and commitment. However, the decision to pool assets is far from straightforward, involving numerous practical, emotional, and legal considerations.

As lifestyles diversify and economic pressures shift, partners are exploring various approaches beyond traditional joint bank accounts. This detailed analysis will help you evaluate whether combining finances suits your unique relationship, detailing the pros and cons, sharing real cases as examples, and exploring modern financial arrangements adopted by contemporary couples.

The Appeal of Combining Finances: Building Financial Unity

Pooling resources is often seen as a sign of cohesion in a relationship. Couples combining finances can benefit from streamlined budgeting, shared responsibility, and greater transparency. Managing expenses like rent, utilities, groceries, and loans becomes simpler when all income is consolidated.

Consider a couple like Emma and David. Both earn moderate salaries and decided early on to open a joint checking account for their monthly expenses. They contribute equal percentages of their income, allowing them to track spending together and plan long-term goals efficiently, such as saving for a home or travel. According to a 2023 study by the National Endowment for Financial Education, couples who share finances report a 20% higher satisfaction rate with their money management practices compared to those who do not.

Combining finances can also position couples better when applying for loans or mortgages. Financial institutions often view joint income favorably, increasing the potential borrowing capacity. This unification can accelerate wealth building, especially when one partner earns significantly more or less than the other, balancing disparities. Furthermore, taxes might be optimized in some jurisdictions by filing jointly, creating additional savings.

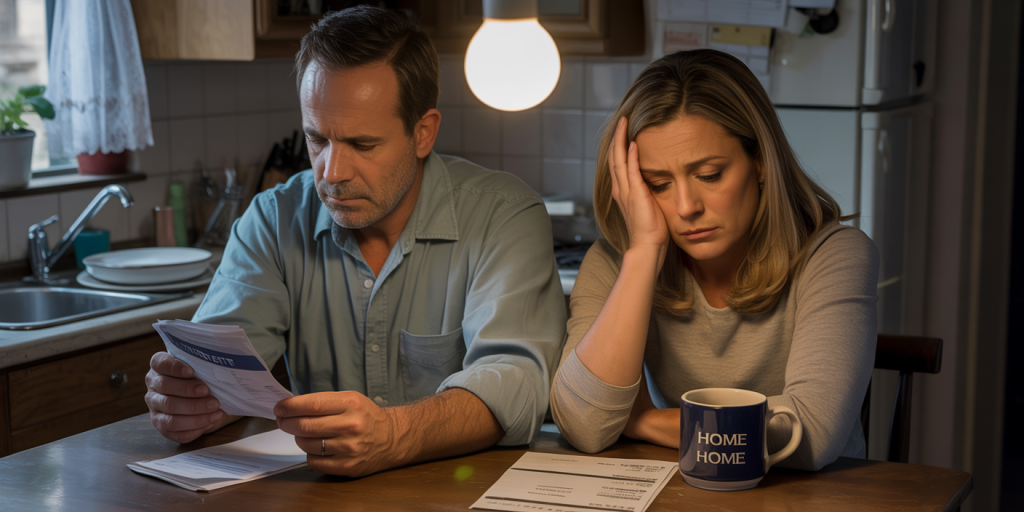

Challenges of Merging Money: Loss of Autonomy and Increased Conflict

Despite its advantages, pooling money carries inherent risks and complications. Many couples find that combining finances exposes them to disagreements over spending habits, saving priorities, and debt management. Loss of financial independence may breed resentment, particularly if one partner feels controlled or scrutinized.

Take the case of Johanna and Mark, who merged accounts after marriage. Mark, a natural saver, found himself frustrated by Johanna’s impulsive purchases. Johanna, on the other hand, felt restricted and less motivated to contribute because she didn’t see the direct benefit of her earnings. Within two years, tension over money grew significant enough to impact their overall relationship.

Another common concern is unequal income contribution. When one partner earns more, questions arise about fairness and balance. How much should each contribute toward household expenses? Is it equitable to divide expenses 50/50, or should it be proportional to income? Without clear communication, such issues can erode trust. Moreover, mixed finances complicate matters during a breakup or divorce, requiring legal intervention to divide shared assets.

Debt is a further sticking point. Merging debts such as student loans and credit cards can entangle both parties financially, making it essential to disclose all liabilities upfront. A 2022 survey by CNBC found that 44% of divorcing couples cited financial issues as a primary cause, with joint debt aggravating the situation.

Alternative Approaches: The Rise of Partial Combining and Customized Systems

Recognizing the challenges of fully merged finances, many couples are now experimenting with hybrid models. These modern alternatives aim to preserve financial independence while capturing some benefits of shared money management.

One common strategy is the “50/50 split” with separate accounts. Each person pays an agreed-upon share of joint expenses—typically proportional to income—to a shared account, while retaining individual discretionary spending. Rachel and Tom adopted this method: Rachel earns 70% of their combined income and Tom 30%. They each deposit their share into the joint account to cover rent, utilities, groceries, and vacations, but keep separate accounts for personal spending without interference.

Another approach is maintaining separate accounts entirely but sharing one specific joint account—for instance, to save for future goals like a wedding or home renovation. This preserves autonomy while encouraging collaboration. This method works well for couples wary of losing control or those in less traditional arrangements, such as partners with vastly different spending philosophies or those wary of legal entanglements.

A comparative overview highlights these methods:

| Approach | Shared Expenses Coverage | Financial Autonomy | Debt Sharing | Complexity | Relationship Transparency |

|---|---|---|---|---|---|

| Full Combined Finances | 100% | Low | Shared | Moderate | High |

| Proportional Shared Account | Major Expenses Only | High | Partial | Low | Moderate |

| Fully Separate Accounts | None | Total | None | Low | Low |

Such flexibility underscores that combining finances is not a one-size-fits-all proposition but one that couples can tailor depending on trust levels, preferences, and financial goals.

Communication and Legal Considerations in Financial Integration

Regardless of the method chosen, open communication is fundamental. Discussing money matters transparently helps partners understand each other’s financial mindset, expectations, and concerns early, averting misunderstandings. Couples are encouraged to have detailed conversations about income, debts, credit scores, spending habits, financial goals, and emergency plans well before merging accounts.

Financial advisors recommend creating a budget together and revisiting it regularly. Wired recently reported a 35% improvement in couple money satisfaction when regular financial check-ins are implemented. These check-ins can dismantle unspoken resentments or surprises.

From a legal perspective, joining finances does not automatically mean equal ownership in all cases. Laws regarding community property or marital assets vary widely. Couples should consult legal professionals to draft agreements such as prenuptial or cohabitation contracts if financial protection is desired. Additionally, joint accounts pose potential risks with creditors if one partner incurs significant debt; creditors may claim joint assets.

In common-law relationships or unmarried partnerships, joint accounts may not confer the same protections as marriage, introducing further complexity. Therefore, understanding your jurisdiction’s rules about financial rights is critical prior to account integration.

Real-World Data and Trends: What Modern Couples Prefer

Recent surveys demonstrate that while many couples still choose full financial integration, a significant and growing portion prefer tailored alternatives. According to a 2023 survey by Mint.com, 42% of respondents said they keep their money mostly separate, while 35% prefer a blended approach, and only 23% opt for fully combined finances.

Millennials and Gen Z couples tend to be more open to hybrid or separate arrangements, reflecting individualistic socio-economic trends and higher awareness of financial independence. Another factor influencing these choices is increased longevity and multiple partnering scenarios, requiring more flexible financial models.

In same-sex marriages and partnerships, financial integration decisions may be influenced by similar factors as opposite-sex couples but also shaped by previous experiences of financial discrimination or legal uncertainty. Regardless of identity, the fundamental principles of trust, transparency, and mutual respect hold.

Future Perspectives: Evolving Technology and Financial Models in Relationships

Looking forward, emerging fintech solutions are set to revolutionize how couples manage shared and individual finances. Applications designed for joint expense tracking, automated proportional bill payments, and personalized budget planning are already gaining traction. Tools like Honeydue or Zeta offer user-friendly interfaces that respect autonomy while promoting collaboration.

Blockchain-based smart contracts could introduce new ways to automate financial agreements between partners securely and transparently, reducing conflict and clarifying obligations. Additionally, AI-driven financial advisors tailored to couples’ behavior and goals may provide custom plans dynamically adapting over time.

Social norms continue to evolve around independence, gender roles, and money management, shifting away from traditional models. This evolution demands adaptable financial structures accommodating diverse partnership forms and life stages.

There is also increasing recognition of financial literacy as a crucial skill for relationship success, leading to more couples engaging in joint education sessions or counseling.

Combining finances with your partner is a nuanced decision that deeply impacts relationship dynamics and future security. Whether opting for full integration or modern alternatives, success depends on clear communication, mutual respect, and careful consideration of both emotional and financial factors. Embracing technology and flexible models provides promising avenues to balance unity with individuality, ensuring money strengthens rather than strains the partnership.