Breaking Free from Debt: A Practical Step-by-Step Plan

Debt has become an increasingly prevalent challenge in modern society. According to a 2023 report by the Federal Reserve, American consumer debt reached a staggering $17.68 trillion, highlighting how pervasive and complex debt can be. Whether it’s credit card debt, student loans, medical bills, or mortgages, managing and ultimately escaping debt requires a structured approach. This article provides a practical step-by-step plan designed to help individuals regain financial freedom, supported by data, real cases, and comparative insights.

Understanding the Debt Landscape

Before tackling debt, it’s crucial to grasp its nature and types. Debt can be broadly categorized into secured and unsecured debt. Secured debts, like mortgages or car loans, are backed by assets, while unsecured debts such as credit cards or personal loans are not. The interest rates and repayment structures vary significantly, influencing how individuals should prioritize repayments.

For instance, the average credit card interest rate in the U.S. hovered around 20.54% in early 2024, according to CreditCards.com, making these debts particularly expensive to maintain. Conversely, mortgage rates, influenced by market trends, averaged 6.5%, which while significant, tend to be lower relative to credit cards and personal loans. Understanding these nuances is fundamental to effective debt management, as it informs where to focus repayment efforts and which debts to restructure first.

Assessing Your Financial Situation Thoroughly

A detailed assessment of your current financial situation is the bedrock of any successful debt repayment plan. Begin by compiling a comprehensive list of all debts, including balances, interest rates, minimum payments, and due dates. This clarity can be illuminating—many people underestimate or lose track of smaller debts that accumulate over time.

Next, evaluate your income sources and monthly expenses. Tracking spending for at least a month using financial management apps like Mint or YNAB (You Need A Budget) can reveal discretionary spending opportunities and wasteful expenses. For example, John, a 35-year-old software engineer from Ohio, discovered he was spending $500 monthly on dining out and subscriptions, funds that, when redirected, accelerated his debt payoff timeline by six months.

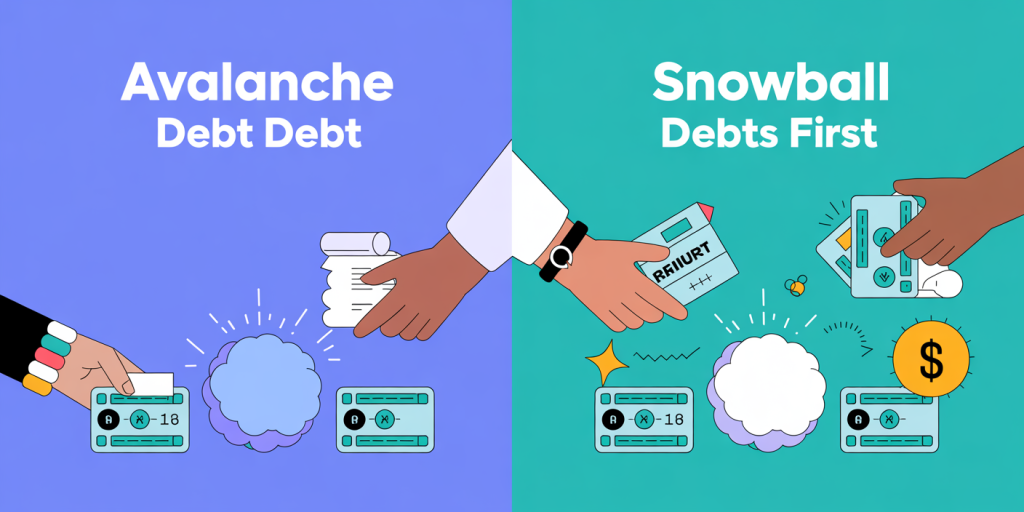

Prioritizing Debt Payments Strategically

Once debts and finances are assessed, the next step is prioritizing repayments using proven techniques. Two of the most popular are the Avalanche and Snowball methods. Avalanche Method: Pay off debts with the highest interest rates first while making minimum payments on others. This method minimizes total interest paid, saving money over time. Snowball Method: Start by paying off the smallest debt first. This builds momentum and motivation by creating a series of quick wins.

| Feature | Avalanche Method | Snowball Method |

|---|---|---|

| Focus | Highest interest rate debts first | Smallest balance debts first |

| Psychological Impact | Less immediate gratification | Builds motivation through early wins |

| Overall Interest Paid | Typically lower | Typically higher |

| Ideal For | Financial planners and disciplined payers | People needing motivation and structure |

Real-world application shows mixed outcomes based on personality and debt profiles. Susan, a teacher from Colorado, used the Snowball Method and reported feeling “empowered and less anxious,” which helped her maintain consistency. On the other hand, Mark, a financial analyst, preferred the Avalanche Method for efficiency and cost-saving.

Creating and Sticking to a Budget

Budgeting is the practical vehicle that drives debt repayment. After identifying non-negotiable expenses—rent, utilities, groceries—focus on trimming or eliminating discretionary spending. Consider reallocating funds from luxuries, like entertainment, towards debt payments. A well-structured budget helps avoid falling back into debt traps.

One powerful approach is the 50/30/20 rule: allocate 50% of your income to essentials, 30% to discretionary spending, and 20% to debt repayments and savings. However, when focused on debt payoff, individuals might temporarily adjust this to a 50/10/40 split, dedicating 40% to aggressively reduce debts.

Practical tools such as Excel-based budgeting sheets or apps like EveryDollar streamline this process. Real-life examples include Clara, a single mother who increased her debt payment percentage by limiting discretionary spending via a digital budget, hitting her goal to be debt-free in under two years.

Negotiating and Consolidating Debt

Sometimes, negotiating with creditors or consolidating multiple debts into a single, lower-interest loan can dramatically improve repayment flexibility. Simple negotiation tactics include requesting lower interest rates or asking for temporary hardship programs.

Debt consolidation options might involve personal loans, balance transfer credit cards, or even home equity loans. For instance, transferring high-interest credit card debt to a card offering a 0% introductory APR can save substantial money if paid off within the promotional period. A comparative table below outlines several consolidation options:

| Debt Consolidation Option | Average Interest Rate | Pros | Cons |

|---|---|---|---|

| Personal Loan | 8-15% | Fixed payment, simpler tracking | May require good credit |

| Balance Transfer Card | 0-3% introductory | Interest-free period, no collateral | High rate after promo ends |

| Home Equity Loan | 6-8% | Lower interest rates, tax benefits | Risk of losing home if default occurs |

Consider Mia, a small business owner from Florida, who consolidated $25,000 in credit card debt with a personal loan at an interest rate 7% lower than her original cards. By cutting down monthly interest by hundreds of dollars, she cleared her debts progressively while managing cash flow for her business.

Building Emergency Savings and Avoiding Future Debt

Breaking free from debt is vital, but equally vital is preventing relapse. Establishing an emergency fund acts as a financial buffer in unexpected circumstances and stops reliance on credit.

Financial experts typically recommend saving three to six months of living expenses. This may feel daunting while repaying debt, but even small consistent contributions can build resilience. For example, the National Foundation for Credit Counseling (NFCC) in 2023 reported that 60% of Americans with emergency funds noted significantly lower incidences of new debt following financial shocks.

Furthermore, improving financial literacy is a long-term investment. Many debt cycles stem from lack of budgeting skills or misunderstanding of interest calculations. Attending workshops, webinars, or even working with financial advisors can transform behaviors and establish a sustainable financial lifestyle.

Future Perspectives on Debt Management

The debt landscape continues evolving influenced by economic conditions, technological advancements, and consumer behaviors. For instance, the rise of fintech solutions and AI-powered budgeting tools democratizes access to personalized financial advice, making debt management more accessible.

Moreover, regulatory changes around interest rate caps and credit transparency may protect consumers from predatory lending. The Consumer Financial Protection Bureau (CFPB) projects increased oversight in the next five years that could shift how unsecured debts, such as payday loans, are managed.

On a personal level, embracing proactive financial habits remains central. Many individuals who once struggled with debt report improved mental health and overall well-being after becoming debt-free, illustrating benefits beyond money itself.

Investing in credit score improvement, leveraging rewards programs, and continuously educating oneself are trends poised to empower a new generation of financially savvy consumers. The journey to debt freedom is challenging but achievable, especially with a practical, data-backed approach tailored to individual circumstances.

—

With these steps and insights, breaking free from debt is not just a dream but a practical goal. Systematic assessment, strategic prioritization, disciplined budgeting, negotiating skills, and financial foresight collectively pave the way to not just resolve current debts but build a foundation for economic stability and freedom.